Calling for automatic release of matured HMRC-allocated Child Trust Funds

There are currently £1 billion of Child Trust Fund birthrights* being denied for young adults in poverty. Delivering HMRC-allocated Child Trust Funds to low-income young adults could be a milestone achievement for Government — it's currently a millstone

“Something that is received or owned especially because of where you were born or your family or social situation, without having to be worked for or bought.”

This opening quotation is a very accurate definition of the birthright which Gordon Brown and Ruth Kelly established for all those children born in the United Kingdom between 1st September 2002 and 2nd January 2011: the Child Trust Fund. Its progressive element even provided a doubling of Government contributions for those born into low-income families.

As at the end of this month, over two-thirds of these young account owners are adults: aged 18 or over — this is the age at which they are entitled to have access to their funds. However, huge numbers of young adults are wholly unaware of their birthright, because their accounts were opened by HM Revenue & Customs: this was because their own family had taken no action to open the account by the child’s first birthday.

28.4% of all Child Trust Funds were opened by this process of HMRC allocation: that's 1,743,000 accounts in total. In the north of England and in the devolved nations, the proportion of HMRC-allocated accounts was nearly one-third (It was over one-third in Scotland and Northern Ireland). In contrast, in the south of England only just over one-fifth of all accounts were opened in this way.

These HMRC-allocated accounts also matter particularly because their proportion of low income recipients is 70% higher than for those accounts which were opened by the child's own family: so, there’s a real concentration in terms of disadvantage. It’s worth noting that all these statistics are derived from Government data.

The Share Foundation is a charity which understands the Child Trust Fund scheme fully: it has already linked over 120,000 young adults to their accounts through its findCTF.sharefound.org search facility, worth over £1/4 billion in total.

The £1 billion figure for unclaimed low-income accounts in the headline above is based on The Share Foundation’s analysis, which also shows that nearly three-quarters of this value is held in these HMRC-allocated accounts. This is why the charity has been pushing so hard for an ‘automatic release’ process (please see the attached description) over the past two years in order to make sure that the money reaches those who need it most.

Both the former Conservative and the present Labour government have so far resisted the introduction of an ‘automatic release’ process at 21 years of age for unclaimed HMRC allocated Child Trust Funds, citing headline reasons of law, data integrity and operations. The Share Foundation continues to work hard to help resolve these concerns, but it's increasingly clear that this resistance is based more on policy procrastination than rational blockages.

On the legal aspects, The Share Foundation has sought legal advice and considers that automatic release is not just lawful, but is required to give effect to the various duties on the The Share Foundation March 2026 gavin.oldham@sharefound.org pg. 1 Government. This is a matter of ongoing engagement, but the simplest way to resolve the dispute would be through ministerial resolve to initiate action.

For the data issues, the fact that all Child Trust Funds are directly referenced by the owner’s National Insurance number enables direct access to up-to-date knowledge of these individuals’ contact information through the benefits, payroll and student loan channels. If it was considered necessary, the automatic release of their funds could easily be preceded with notification of their imminent arrival if this was considered a preferred approach.

From the operational perspective, The Share Foundation has volunteered to carry out the work involved! However before it can be set in motion, identification of which are HMRC allocated unclaimed accounts being administered by account providers will have to be established: notwithstanding HMRC’s ‘settlor’ role, this was not a regulatory requirement throughout the past 23 years and it needs a comprehensive checking process. In December 2025, HM Treasury and HMRC undertook to do this work, but as yet no action has been taken — again, there is clearly insufficient policy prioritisation.

The Share Foundation is particularly keen to work co-operatively with Government to move this issue forward and to enable these young adult owners to have access to their birthright Child Trust Funds. Thus far, it has had to resort to a proposed legal ‘Judicial Review’ process to achieve any element of substantive Government involvement.

It is strange to find a Government which, while it expresses such concern over the poverty of young people, at the same time is doing so little to deliver on the ground-breaking Child Trust Fund scheme introduced by the previous Labour Government.

The Share Foundation has established that there are no irreconcilable impediments in terms of legal, data or operational aspects: so, we must conclude that the ‘number one’ problem is policy procrastination. That is absolutely not fair on these hundreds of thousands of young adults from low-income backgrounds.

So, what should be done next? The charity could embark on a lengthy legal process, and it would probably succeed; but this would set the whole timeline back, potentially for years. These young people can't afford to be denied their birthright for so long, quite apart from the negative consequences of having to resort to such a confrontational approach.

If it is correct to conclude that the main task is to raise policy prioritisation, perhaps it will be necessary to build further support across Parliament, and to increase awareness across the north of England and the devolved nations, as it is their young adults which are particularly disadvantaged by this policy procrastination.

The right way forward must be found.

However, there is no doubt that the birthright which Gordon Brown and Ruth Kelly set in place for low-income young people must be delivered, and this is particularly the case for those Child Trust Funds where Government was — and still is — settlor for the accounts.

Gavin Oldham OBE

Chair of Trustees

The Share Foundation

HMRC-Allocated matured Child Trust Funds (CTFs)

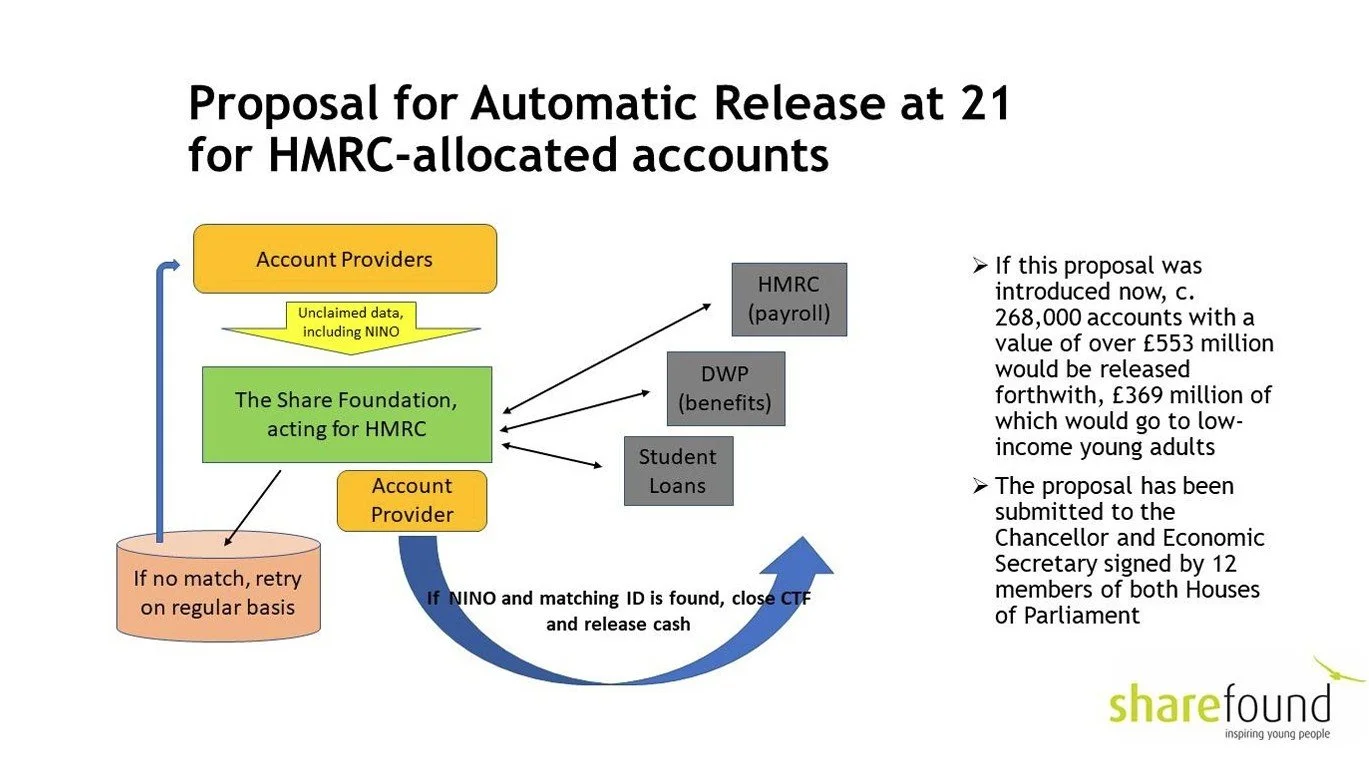

This is the proposal for a new process for requiring CTF account providers to close and pay out the proceeds via HMRC where possible to all young adult owners of HMRC-allocated matured CTFs which remain unclaimed and unregistered as at a young adult’s 21st birthday.

The logic is that, unlike family-opened accounts, in most cases there is no evidence that the young person or their family has ever been aware of their HMRC-allocated account and, because of the close correlation between these recipients and ‘low income’ status, the proceeds are much needed in order to provide an improved start to adult life. Because HMRC opened the account in the first place, it is therefore appropriate that HMRC should enable the proceeds to be delivered.

The Share Foundation have reliable information that over 46% of adult-owned HMRC-allocated CTFs are unclaimed. This process, which would allow three years for a young person to claim or manage their account at their own volition, would therefore enable c. 268,000 accounts to be released immediately, 51% of which are owned by low-income young adults, the most disadvantaged. We estimate that it would release c. £553 million immediately followed by c. £18 million per month (£0.21 billion p.a), thus significantly relieving cost of living pressures.

The process would be as follows:

CTF account providers with beneficial account owners who had reached their 21st birthday would identify these accounts and notify HMRC of their identity, including their National Insurance number.

HMRC would establish whether those individuals feature as benefit recipients, via a company payroll or in the student loan system, or through any other current relationship involving receipt from or payment to government. HMRC would then confirm to the account provider that these accounts should be closed and the proceeds paid to an HMRC transfer account for onwards payment as appropriate. HMRC would, if at all possible, notify the young adults of their impending receipt.

All identified accounts for which HMRC have no current links would be informed as such to the account provider, who would re-test on a quarterly basis going forwards.

Statistics would be published quarterly to provide progress information for all parties helping to reconnect unclaimed Child Trust Funds.

There should be provision for CTF status to be restored in the event of a young adult requesting it. However, because these HMRC-allocated accounts are so focused on the most disadvantaged, it is very unlikely that this would apply — across all matured CTFs the retention rate is only 6%.

Gavin Oldham OBE

The Share Foundation gavin.oldham@sharefound.org